It is common knowledge that small businesses have a hard time qualifying for traditional bank loans. That is why many of them turn to alternative lenders. Alternative lending institutions offer an easier way for small enterprises to get the funds they need to put towards business initiatives – be it marketing, renovations, expansion, or even day-to-day expenses.

If you find yourself always dealing with outstanding invoices from time to time that it’s starting to affect your business’ cash flow, you will need some help. Invoice financing is one alternative lending option that SME’s can turn to if they’re having difficulty making ends meet.

In this article, we’ll help you learn more about invoice financing. With that, here’s an overview of what invoice financing is, how it works, and its benefits.

What is Invoice Financing?

Invoice financing is a type of financing wherein the lenders ‘purchases’ a business’ invoices or account receivables. The businesses, in turn, gets funding in exchange. You and the financing company can come up with an agreement on the collection of the payments. The financing company can take full control of the ledger and handle payment collection, or the business can retain full control of the ledger and pay the invoice financing company.

In other words, you won’t have to wait for 30, 60, or 90 days for your customers to pay you. With invoice financing, you’ll get the cash upfront, which you can then put towards any business needs.

How It Works

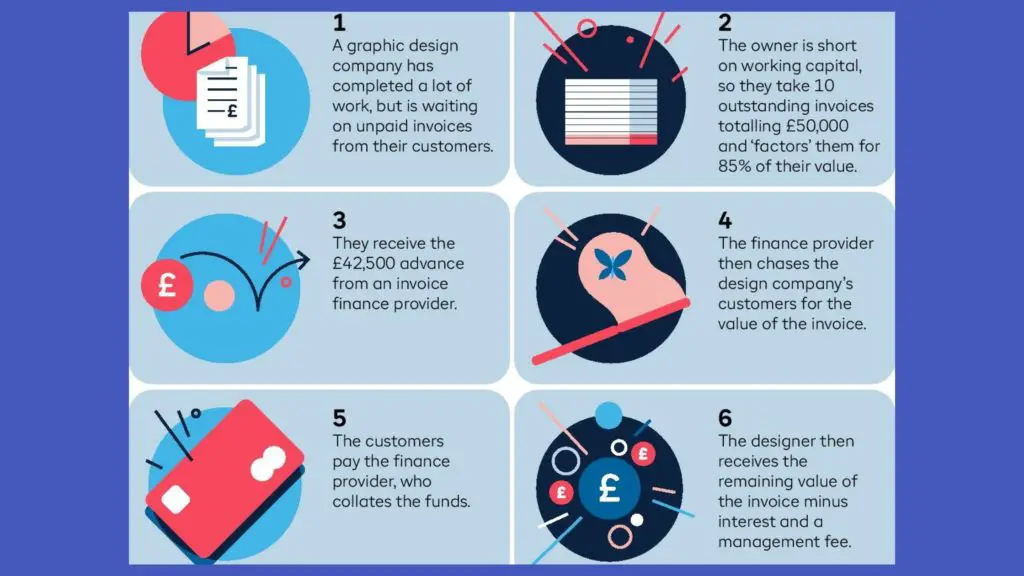

There are three key players involved in invoice financing: the merchant (borrower), invoice financing provider (lender), and the customers. If a merchant finds that they’re experiencing cash flow issues because of uncollected payments from their customers, they turn to the invoice financing companies for help.

The process starts with the merchants selling their invoice ledger to the financing company. The company then assesses the risk involved by looking into the customers of the merchant. They factor in the customers’ financial and credit background. If they find it satisfactory, only then will they can grant the financing to the merchants.

The merchants get the money upfront – usually, 80% to 95% of the invoices financed. Once the customers settle their accounts, the invoice financing company then deducts their share and returns the remaining balance to the merchants.

What are the Benefits of Invoice Financing?

There are a lot of reasons why business owners apply for financing. Here are the benefits of invoice financing for businesses:

1. High Approval Rates

Unlike traditional loans where they put emphasis on the credit background of the borrowers, invoice financing companies don’t consider that as significant considerations for approval. Since the invoices are really all that matters, the financing company looks at the merchant’s customers’ credit background and payment history instead. As long as your customers have a decent financial background, then your chances for approval are higher.

2. Immediate Cash Flow Solution

Applying for traditional financing can be long and tedious. Approval could take 60 to 90 days. In some cases, it could even take as long as six months. If your business needs fast cash, then going this route isn’t the best way to go.

On the other hand, invoice financing can get you the funding you need within days after your application. Once the company confirms your customers’ credibility, you can get the cash immediately, ensuring that your business runs smoothly.

3. You Won’t Have to Worry About Payment Collection

A type of invoice financing, called invoice factoring, requires you to give up control of your ledgers to the financing company. With that, they will also be the ones to handle the payment collection. If your company doesn’t have the resources to constantly chase customers for payments, then invoice factoring would be a viable financing choice for your business.

What are the Downsides of Invoice Financing?

While invoice financing does offer incredible benefits to the merchants, it does have its downsides like every other financing option.

It’s More Expensive than Traditional Loans

Invoice financing companies face a high risk of letting you borrow money. It is for that reason that they set high fees. Charging higher fees to their customers acts as the cushion for the risk they’re taking. If cost is an issue for you, then invoice financing may not be your best financing choice. Other financing options like business credit cards and lines of credit could be a viable alternative.

Less Privacy

As mentioned in invoice factoring, the financing company will assume the payment collection. With that, your customers are more likely to know your relationship with the financing company since they’ll be paying there directly. This can be uncomfortable for some small business owners as this may make their customers think that they’re experiencing financial issues, thus negatively affecting their business relationships.

Should You Choose Invoice Financing?

Invoice financing can be a useful resource to small business owners needing an extra cash flow boost. However, be sure to learn more about invoice financing before diving in headfirst. Like any other financial options, invoice financing has its pros and cons. Consider the needs and your business situation first. Do you need quick cash? Can you afford the high fees? Is privacy not a problem for you? If so, then invoice financing might just be the financing solution for you.